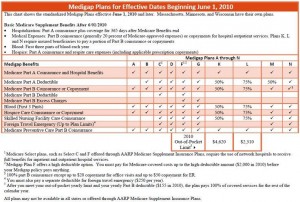

Medigap Plan F is the most common and comprehensive Medigap plan. This plan pays everything that Medicare Parts A and B do not pay at the doctor and hospital so that you do not have any out-of-pocket costs. A recent study of the industry found that over 50% of people who have a Medigap policy currently have Medigap Plan F.

Below is a list of the things that Medigap Plan F covers:

- Medicare Part A coinsurance (the 20% Medicare does not pay)

- Medicare Part A hospital costs (additional 365 days after Medicare benefits are used)

- Medicare Part B coinsurance (the 20% Medicare does not pay)

- Blood (first 3 pints)

- Medicare Part A hospice care coinsurance (the 20% that Medicare does not pay)

- Skilled nursing facility coinsurance (the 20% that Medicare does not cover)

- Part A deductible (currently $1316/benefit period)

- Part B deductible (currently $183/year)

- Part B excess charges (when a doctor charges more than Medicare’s normal fee schedule)

- Foreign travel emergency

These can also be found on the Medigap coverage chart.

People who choose Plan F often do so because of the predictability that it brings. It is a way to “fix” your insurance costs that meshes well with a “fixed” income. Most companies do offer Plan F since it is the most common plan.

So, it is easy to find this plan easy to compare one companies’ Plan F with the Plan F from a different company. Medigap plans are Federally-standardized; that is, they are required to offer the benefits from the Medigap coverage chart above. A Plan F, regardless of what company it is purchased from, will always cover the list of benefits mentioned above. However, rates for Plan F (and other plans) can vary considerably from one insurance company to another. Because of this variation, it is crucial to compare Plan F rates on the basis of price and company reputation.

Although Plan F has all of these things in its favor – predictability of costs, most common plan, offered by most companies, easy to understand and compare – it is not always the best “deal”. Plan G is the next step down from Plan F and also offers similarly predictable out of pocket costs and is a lower premium plan. The only benefit from the list above that is NOT a part of Plan G is the coverage for the Medicare Part B deductible, which is currently $183/year (for 2017). It is advisable to compare premiums on both of these plans, because if the premiums for Plan G are significantly lower than those for Plan F, it may make sense to go with the lower-premium Plan G.

most companies, easy to understand and compare – it is not always the best “deal”. Plan G is the next step down from Plan F and also offers similarly predictable out of pocket costs and is a lower premium plan. The only benefit from the list above that is NOT a part of Plan G is the coverage for the Medicare Part B deductible, which is currently $183/year (for 2017). It is advisable to compare premiums on both of these plans, because if the premiums for Plan G are significantly lower than those for Plan F, it may make sense to go with the lower-premium Plan G.

Regardless of whether you pick Plan F or Plan G, and regardless of which company you choose, all Medigap plans can be used at any doctor or hospital that takes Medicare nationwide. One of the most common questions, when it comes to aging in to Medicare or even for people already on Medicare, is whether your doctor or hospital will take plans from a certain company. However, because Medicare is your primary coverage, the Medigap plans “follow” Medicare. If Medicare is accepted, the doctor or hospital will also take your Medigap plan. If a provider is non-participating in Medicare, likewise, your Medigap plan won’t help.

This is an important differentiation between Medigap plans and Medicare replacement plans, such as Medicare Advantage. Medicare Advantage plans are either PPOs or HMOs in most cases, meaning that they have a set, regionally-defined network that you must stay within. Doctors/hospitals can choose, sometimes on a case-by-case basis, whether or not they are going to accept your plan.

Medigap Plan F is definitely a plan to consider if you are someone enticed by predictability and consistency, although you certainly should evaluate premiums of other lower premium options, such as Plan G or Plan N.

If you have questions about this information or would like more information, please contact us on our website or call us at 877.506.3378.